Africa’s Housing Finance Markets in 2015

Innovation in housing finance –in terms of products, players, and approaches, not to mention target markets – is a key feature across the continent, creating new opportunities for investment and delivery.

As both local and international investors chase growth opportunities in a sluggish global economy, they are employing diversification strategies to manage the risks of their traditional targets – and in this, residential property is increasingly becoming an option. And while established players are getting better at what they do, new players are adding to the mix and competing for opportunities.

nvestors are faced with a paradox, however. By their very nature, they are drawn to the high income markets. It is in these markets that they can price adequately for risk and realize the returns they seek. However, the real story – the scale opportunity just waiting to be cracked – is in the lower income market segments. The arguments for investment in residential – high urbanization rates, a growing middle class, a shortage of supply – these are all arguments for moving down market into the uncharted waters of affordable housing. Can investors and developers do it? In 2015, this is a very real focus.

Of course, the challenges are not insignificant, and cannot be easily wished away. But increasingly, investors and developers are noting that the potential benefits outweigh the risks. And, as governments come to appreciate the potential that this interest offers, their efforts to streamline development processes and enable their local housing markets to grow are creating new opportunities that are beginning to change the face of African cities.

A key challenge facing investors has been the inability to find investment targets in the residential real estate space that are sufficiently substantial to warrant their attention. International and local institutional investors generally seek large investment targets where they can place their money and realize a steady return that isn’t drained by the administrative and organizational weight of multiple projects. With the exception of South Africa, African housing markets lack the capacity to receive big money. Developers haven’t the capacity to build housing at scale and municipalities haven’t the capacity to receive large scale housing developments. Some investors are noting a change, however: investment in large scale infrastructure – roads, energy, even telecommunications – clears the way and reduces some of the transaction costs associated with housing developments. As the African head of Real Estate Finance for Standard Bank, Gerhard Zeelie, says “economic growth and ongoing investments in infrastructure are opening up previously inaccessible markets.”

Given this, investors have been looking for innovative ways to make the connection between their capital and potential investment opportunities. The introduction of Real Estate Investment Trusts (REITs) is perhaps the most significant of these – these create a vehicle that investors understand and can trust, aggregating diverse sources of funding from international and institutional investors through to households, and targeting them into a portfolio that extends beyond the limitations of individual projects.

REITs are new in Africa – having developed through the promulgation of legislation and issuing of regulations only in the past three years, in South Africa, Nigeria, Tanzania, Kenya, Ghana, Morocco, and Zimbabwe. Initially used for the retail and commercial real estate sectors, residential REITs are now also emerging. The first residential-only REIT in South Africa, Indluplace, listed on the Johannesburg Stock Exchange in June 2015. Promoted by Arrowhead Properties, which has been bringing residential properties into its REIT portfolios since 2013, Indluplace focuses on affordable rental.

In some jurisdictions, the REIT legislation allows for a housing development focus. This was a Kenyan innovation, which allows for the Development REIT (D-REIT). Investors take some of the project risk, so the regulations limit D-REITs to professional investors. A D-REIT can be converted into an Income REIT (I-REIT) which realizes returns through rental cash flows, when the bulk of the assets have completed the construction phase and rentals begin to flow. In Tanzania, the Capital Markets and Securities Authority (CMSA) approved Watumishi Housing Company REIT in early 2015. WHC-REIT aims to mobilise funding for the development of low-middle income housing, both for sale and for rent, and the development of commercial properties.

Another innovation whose practice has been evolving as its been tried in different countries, is the mortgage liquidity facility. Originally introduced in Africa with the establishment of the Egyptian Mortgage Refinancing Company in 2007, this was soon followed by the establishment of the Tanzania Mortgage Refinance Company in 2010, the Caisse Regional de Refinancement Hypothecaire-UEMOA in 2012, and the Nigerian Mortgage Refinance Company in 2014. While there are variations from one to the next, the model essentially allows for the liquidity facility to purchase mortgages from mortgage lenders, giving them the liquidity to fund further mortgages. In order to engage with multiple lenders, the facility requires standardization of mortgages, which over time makes them more accessible to investors.

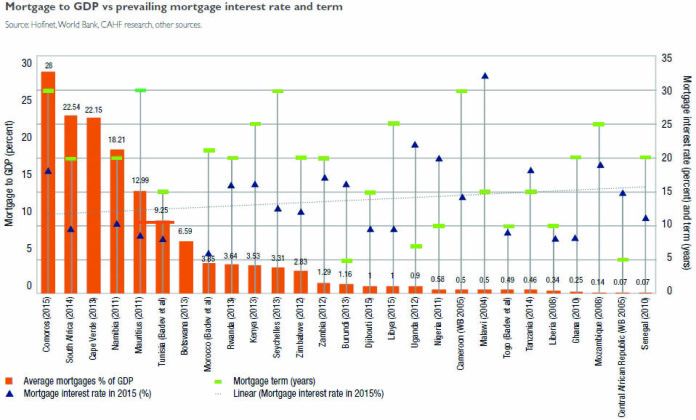

Of course, mortgages are only feasible when they’re affordable. Mortgage rates above fifteen percent, and offered at tenors below ten years, are unhelpful. Beyond the factors that liquidity facilities address, macro-economic factors – the pricing of Treasury Bill rates, inflation, the availability of long term capital, the strength of capital markets, and so on – are behind a lender’s ability to make the mortgage work. In Malawi, a borrower might as well buy their house with their credit card. It is unsurprising therefore, that mortgages comprise only 0.5 percent of GDP. Interestingly, a number of countries are offering mortgages at rates below 15 percent and for tenors over 15 years, and some now at even less than 10 percent and over 20 years.

Download graph

Since the early “Africa rising” narrative, analysts have been citing the potential to be found in a young, growing middle class becoming economic participants in countries where the rate of urbanisation outpaces the rate of population growth. This, together with the commodities boom, spurred investment in infrastructure, which then facilitated investment in real estate – largely commercial and retail. In 2014, foreign direct investment into real estate was second behind coal, oil and natural gas, comprising 14 percent market share and US$12 billion. South African retailers pushed north into Zambia, Botswana, Mozambique, Tanzania, Kenya, Nigeria, Ghana, seeking new markets. New shopping malls were opened, and the “African real estate market” became a focus of more detailed analysis and investor interest. With the commodities downturn, the fall in the oil price, and the depreciation of many local currencies against the strengthening dollar, however, investors are being forced to diversify their strategies. Their local experience has shown them the housing backlogs that beset virtually all African cities, and while they now have a better understanding of the target market, residential becomes a new opportunity.

The identification of niche markets and an appreciation of the affordability challenge: And yet, the enthusiasm with residential will be misplaced if it is only focused on the top end. The bulk of the backlog is not in the high end property market, but rather in what is being called the affordable market – home to new entrants to the middle class. Affordability is higher in urban areas, of course, where residents are more likely to have an income stream that can support a long term mortgage obligation – but even so, less than ten percent of households across the continent are likely to afford a mortgage for even the cheapest, newly built house, built by a private developer.

Download graph

Given these affordability challenges, and the very real need and obvious demand for housing, investors and developers are targeting specific niche markets that pull together resources in innovative ways. An important niche is the rental market. This was the focus of two recent symposia hosted by development financier Shelter Afrique this year, one of which was in Ghana. Across these two events, proponents highlighted the opportunity for regular cash flow and increasing rentals as a hedge against the long term expectation for property appreciation. The rental sector offers strong synergies with pension fund liabilities, and provides opportunities for diversification. Demand is obvious: Africa’s cities are welcoming streams of new migrants, and the middle class is young and both upwardly and geographically mobile in their pursuit of employment. This, plus the simple absence of housing for ownership, makes rental an obvious target. And critically, a growing track record is showing impressive results.

Within the rental sector, student housing has been a critically overlooked housing niche. A key challenge in making this market segment work, has been the need for property managers that are specialist in this market segment. As the demand for diversification shifts practitioners in the direction of residential, however, the student niche offers a focus that is attracting some investors. In many countries, housing investors are targeting employers, whether public or private, as critical role players that can facilitate their workers’ access to the resources they need to pay for their housing. In South Africa, Pretoria Portland Cement has embarked on a “Home Owners Support Programme”, assisting low income employees to improve their housing circumstances. Certainly, a key determinant of market demand is income – both in terms of quantum and source. The graphs that follow provide an indication of the nuance of this demand. This sort of market segmentation can enable a more careful targeting, and changes the affordability challenge. Download graph

A further perspective. The housing affordability story is significantly influenced by the price of building materials, and this is an issue that the Centre for Affordable Housing Finance in Africa (CAHF) is exploring with its partners in the coming year. Key among these is the price of cement. If it takes 35-40 bags of cement for the construction of a 40m2 brick and mortar house, the per bag cost is a critical factor. In 2015, the most expensive country with respect to cement, at US$30,30 for a 50kg bag, was the DRC, followed closely by South Sudan, where the same bag cost US$29,00. Compare this with Nigeria (US$11,00), Kenya (US$7,60), and Senegal (US$5,06), and the cheapest source of cement, Tunisia (US$3,53), and the capacity of a household to build their home with cement becomes somewhat more clear.

Policy & regulatory evolution to match investor interest: Even in 2015, the key challenge that investors and developers highlight from their experiences across the continent, and including South Africa, is regulatory and policy uncertainty and instability. This factor is critically important because of the long term nature of housing investments. Unpredictable regulatory changes, complex legal frameworks and volatile local currencies all limit investment timeframes and challenge exit strategies, encouraging investors to look elsewhere while governments get their house in order, so to speak. Government policy can have a significant impact on investor interest and market participation, simply by being reliable.

Access to land is a key factor, and regulatory challenges in this regard also undermine the capacity to deliver at scale. At the I H S affordable housing summit, a Nigerian developer, Resilient Africa, reported that of the ZAR28 billion (US$ 2.139 billion) worth of ‘large lot size property’ sold across the continent in 2014, ZAR26 billion (US$1.986 billion) was in South Africa. The ability to acquire large tracts of land for property development is constrained in very many jurisdictions by the capacity of local governments to package and present that land as required by legislation – and to administer and manage it over time, thereafter.

Ironically, Kenyan REIT legislation requires that the property development option (the D-REIT) is restricted to 15 percent of the REIT value to help manage the risks – many of which are regulatory in nature. If REITs are to have a significant impact on the financing of housing development, governments must focus on the risks inherent in the development process, which undermine investment, or at best, make it more expensive. And they are. A key indicator offered by the World Bank as part of its “doing business indicators” is the number of days and cost involved to register property (a commercial property, in this instance, but indicative nonetheless). Comparing data from 2012 and 2015, it is clear that there have been improvements: Rwanda, Burundi, Morocco, Lesotho, Cote d’Ivoire, Guinea-Bissau, Sierra Leone, and Senegal have all shown noticeable improvements in the time it takes to register a property, with Guinea-Bissau being the star performer. The cost of registering property in Zambia and Namibia increased in the period.

Growing experience and investor sophistication: It’s worth noting that investors who have lasted this long aren’t frightened – and the potential returns are enough to keep them focused on the long haul. In June 2014, private equity investor I H S announced the first close of their second fund, following the strong, risk-adjusted returns achieved in its first fund, worth ZAR1,8 billion, which provided financing for over 28 000 units across South Africa. Announcing their second fund, I H S said that the strong returns achieved with the first fund provided clear proof that the affordable housing market, targeted at middle and low income earners, was a sound investment, and a strong base for ongoing inflows into the sector.

A separate example is that of Housing Finance Kenya, a leading mortgage provider in Kenya. Over the course of its operations, from its founding in 1965 by the Commonwealth Development Corporation (CDC) and the Government of Kenya, to its listing on the Nairobi stock exchange in 1992, to issuing Rights Issues of Shares and a Corporate Bond, to launching the HF Group, an integrated property, banking and investment solutions company, in 2015, HF Kenya has increasingly engaged with the capital market. Its first bond issue in 2010 was hugely oversubscribed, demonstrating investor confidence in the focus and operations of this company which targeted the residential real estate market in Kenya.

These experiences are not lost on investors, and the success of companies like the HF Group bode well for other players also operating in the market and seeking market participation in their activities. The value of local currencies has also fallen – in Ghana, by as much as 50 percent. And political instability in many regions has made any sort of investment much more difficult. These factors haven’t changed the reality of an affordable housing shortage, however, and may well be stimulating investors and developers to think differently about what and to whom they deliver. The space for conversation is certainly opening up. – First published in the Housing Finance in Africa Yearbook 2015.

http://www.housingfinanceafrica.org